When it comes to managing your personal finances, few things are as critical as staying on top of your insurance coverage. Whether it’s auto, health, home, or life insurance, every policy comes with a fixed term—and when that term ends, you’ll receive a renewal notice. Understanding this document can help you avoid coverage lapses, premium hikes, and missed opportunities for better coverage. In this guide, we’ll break down everything you need to know about an insurance renewal notice and how to take control of your coverage.

What Is an Insurance Renewal Notice?

An insurance renewal notice is a formal document sent by your insurer notifying you that your current insurance policy is about to expire. It outlines the terms for continuing your policy, including the premium for the new term, any changes to coverage, and the renewal date.

When Do You Receive It?

Typically, renewal notices are sent 30 to 60 days before your policy expires. This gives you ample time to review the terms and make any necessary changes.

Why Is It Important?

Ignoring a renewal notice can lead to coverage lapses, automatic renewals with higher premiums, or the continuation of a policy that no longer meets your needs.

Key Components of an Insurance Renewal Notice

Every insurer may format renewal notices differently, but most include the following critical components:

1. Policy Summary

This includes your current coverage details, such as:

- Type of insurance

- Policy number

- Coverage limits

- Deductibles

- Term dates

2. Renewal Terms

This section details:

- The new policy period

- Adjustments to premiums

- Any changes in terms or benefits

- Renewal options (automatic or manual)

3. Premium Information

Here, you’ll see the new premium amount, how it’s calculated, and available payment plans (monthly, quarterly, annually).

4. Discounts and Surcharges

Any applicable discounts (e.g., safe driver, no-claim bonus) or added fees due to prior claims or risk factors will be highlighted here.

5. Action Required

This outlines what you must do to maintain or cancel the policy, including:

- Paying the premium

- Signing and returning the notice (if required)

- Contacting your agent or insurer for changes

Types of Insurance Renewal Notices

Each type of insurance comes with its own renewal considerations. Here’s how renewal notices differ based on policy type:

Auto Insurance

Auto insurance renewal notices often include:

- Driving history adjustments

- Claim history impact

- Vehicle information updates

Health Insurance

Key elements in health insurance renewals:

- Premium increases

- Changes in network providers

- New co-pay or deductible amounts

Home Insurance

These notices may reflect:

- Property value reassessments

- Risk zone reclassifications

- Added endorsements (e.g., natural disasters)

Life Insurance

Life insurance renewal notices are usually for term policies, showing:

- New premiums based on age

- Renewal options (convert to whole life, extend term)

- Beneficiary updates

Common Changes in Renewal Notices

It’s important to carefully read the renewal notice for any of the following:

Premium Increases

Insurance companies may raise premiums due to:

- Inflation

- Claims history

- Market conditions

- Risk reassessment

Changes in Coverage

Insurers might adjust coverage limits, exclusions, or add new clauses. These changes can impact your protection significantly.

Updated Terms and Conditions

Policy language might evolve, especially due to new regulations or laws, which could affect how and when claims are paid.

What to Do When You Receive a Renewal Notice

Step 1: Read It Thoroughly

Don’t just skim the notice. Read each section carefully to understand changes and new obligations.

Step 2: Compare Your Current Coverage

Ask yourself:

- Is my coverage still adequate?

- Have my needs changed?

- Am I overpaying?

Step 3: Shop Around

Use the renewal period as an opportunity to compare quotes from other insurers. This helps you make informed decisions and potentially save money.

Step 4: Contact Your Insurer or Agent

If you have questions or want to adjust your coverage, now is the time to speak with your provider.

Step 5: Take Action Before the Deadline

Missing the renewal deadline may lead to:

- Policy cancellation

- Higher rates upon reinstatement

- Gaps in coverage

Tips for Managing Insurance Renewals

Set Calendar Reminders

Add reminders for renewal dates so you’re not caught off guard.

Bundle Policies

Bundling (e.g., home and auto) may help you qualify for discounts and streamline renewals.

Keep Personal Information Updated

Incorrect data can lead to wrong premium calculations or missed communications.

Maintain a Claims-Free Record

The fewer claims you make, the lower your risk profile—translating to better renewal offers.

Conduct Annual Policy Reviews

Even if your policy auto-renews, conduct an annual review to ensure your coverage meets your current lifestyle and financial goals.

What If You Miss the Renewal Notice?

Grace Periods

Some insurers offer grace periods—short extensions (usually 7–30 days) during which you can renew your policy without penalties.

Reinstatement Options

If your policy has lapsed, your insurer may allow reinstatement, sometimes with late fees or a health/vehicle inspection.

Shopping for New Coverage

If reinstatement isn’t possible, compare quotes immediately and secure new coverage before driving or exposing assets.

Pros and Cons of Automatic Renewal

Pros

- Convenience

- Continuous coverage

- Avoids unintentional lapses

Cons

- Potential premium hikes go unnoticed

- Missed opportunity to explore better deals

- May continue outdated or unnecessary coverage

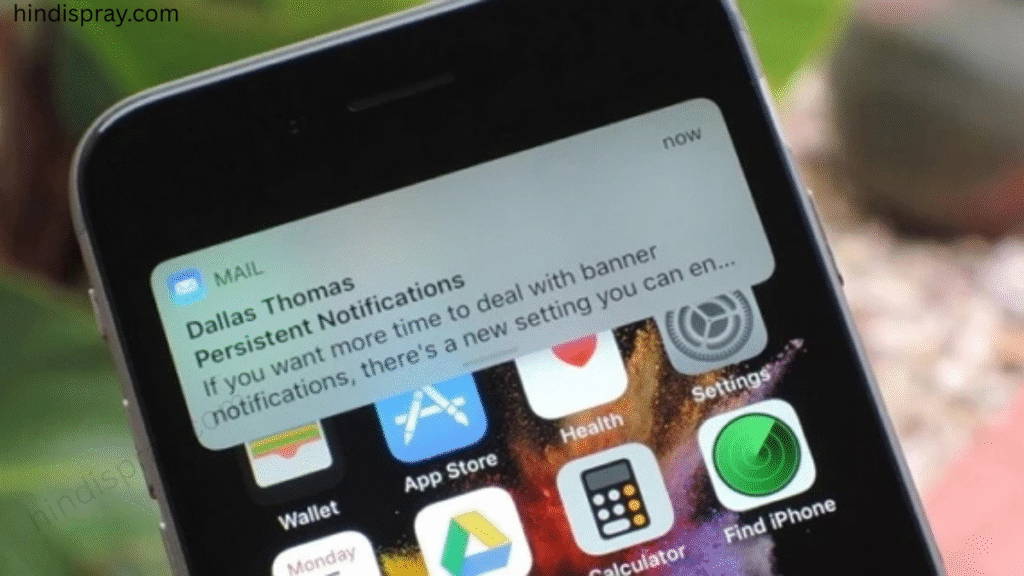

Digital Insurance Renewal Notices

Email and Mobile Notifications

Many insurers now send renewal notices via email or mobile apps. Ensure your contact details are current.

Online Policy Management

Log in to your insurer’s dashboard to:

- Review and accept renewal terms

- Modify coverage

- Download policy documents

Regulatory Aspects and Consumer Rights

In many countries, insurers are legally required to provide advance notice before renewing or altering terms. You also have:

- The right to cancel anytime

- The right to receive a refund for unused premiums

- The right to request detailed policy explanations

Also Read: How To Create An Effective Insurance Marketing Plan?

Conclusion

Insurance renewal notices are more than just a routine formality—they’re a crucial checkpoint in your financial planning. Ignoring them can cost you money, lead to inadequate coverage, or cause your policy to lapse. By understanding what’s included in a renewal notice and taking timely action, you stay in control of your financial security. Make it a habit to review your renewal documents each year, ask questions, and compare offers—because when it comes to insurance, being proactive pays off.

FAQs

1. What happens if I ignore my insurance renewal notice?

If you ignore the notice, your policy could auto-renew with new terms or lapse entirely, leaving you uninsured and possibly facing penalties or legal issues.

2. Can I negotiate the premium mentioned in my renewal notice?

Yes, you can often discuss premium adjustments with your insurer, especially if you have a good record or changes in risk factors (like fewer miles driven).

3. Do all insurance policies auto-renew?

Not all. Some policies require manual renewal or signatures. Always read your notice to understand the specific requirements.

4. Can I switch insurers after receiving a renewal notice?

Absolutely. You’re not obligated to renew with the same provider. Use the renewal period to compare offers and switch if needed.

5. How do I know if my policy has changed during renewal?

Your renewal notice will highlight any changes to coverage, premiums, terms, or benefits. Review it line by line and contact your insurer if unsure.